Navigating volatility: How to stay confident when markets feel uncertain

Markets may feel more restless than ever, but the secret to long-term success isn’t avoiding the waves—it’s learning how to ride them. Dive into the historical patterns of market resilience and discover how a disciplined strategy can turn today’s "noise" into tomorrow’s growth.

If markets feel unusually restless today, it’s understandable. A range of economic, geopolitical and policy-related forces is weighing on investor confidence all at once. The news cycle itself can often intensify the effect, making every market move feel like a crisis or turning point.

Yet here's the reassuring truth: market volatility is a normal part of long-term investing. What’s different today is not the presence of volatility but the sheer speed and volume of information that surrounds it. Filtering out this short-term noise reveals a historical, enduring pattern: markets trend upward over time, carried by companies that grow, adapt and generate durable earnings.

Historically, long-term investment success has less to do with avoiding volatility than with managing through it steadily. Discipline, diversification and a commitment to staying invested during difficult periods tend to make the difference over time.

What’s really causing today’s market ups and downs?

Not all market volatility reflects what’s actually happening in the economy. Much of it is driven by investor sentiment—the collective mood of the market—rather than shifts in company fundamentals. Sentiment can change quickly, particularly in an environment where headlines are constant and often framed around risk rather than opportunity. Some of these short-term sentiment pressures include:

- Caution amid geopolitical tensions: Markets don’t require a full‑blown geopolitical crisis to react. Even the potential for disruptions to energy, trade routes or supply chains can be enough to prompt investors to lean more defensive.

- Fast, polarized news cycles: Markets respond not only to data but to the narrative surrounding it. Today’s dramatic headlines and continuous commentary can amplify concerns well beyond what the fundamentals justify.

- Uncertainty of trade, tariffs and policy: The rise of protectionist trade policies and tariff threats has added a new layer of unpredictability. Markets tend to react to the prospect of these measures as much as to the measures themselves.

- Politics and the cost of not knowing: Election periods tend to bring hesitation rather than lasting damage. Markets have historically struggled more with the uncertainty leading up to an election than with the outcome itself.

Regardless of what factors lead to volatility, the good news is that company earnings typically remain the most reliable long-term anchor for markets. While volatility can dominate headlines, it often has little to do with the true financial health of businesses.

What history shows us: Markets recover, even when it doesn’t feel like it

Every period of stress feels exceptional in the moment. But looking back, the pattern is consistent. Markets have recovered from every downturn, often sooner than expected.

- Global Financial Crisis (2008–2009): The cost of abandoning a plan

Selling felt prudent at the time, yet many who exited missed a substantial recovery. Remaining invested proved more effective than reacting to fear. - COVID‑19 Shock (2020): Waiting for comfort is expensive

Markets fell sharply but rebounded quickly, well before the broader economy regained its footing. - Inflation‑driven turmoil (2022–2023): When the rulebook changes

Both stocks and bonds struggled, underscoring the need for broad diversification rather than reliance on any single asset class. - Dot‑com bust (early 2000s): Getting paid to wait

During years of slow equity progress, dividends and income played a stabilizing role, demonstrating the importance of total-return thinking.

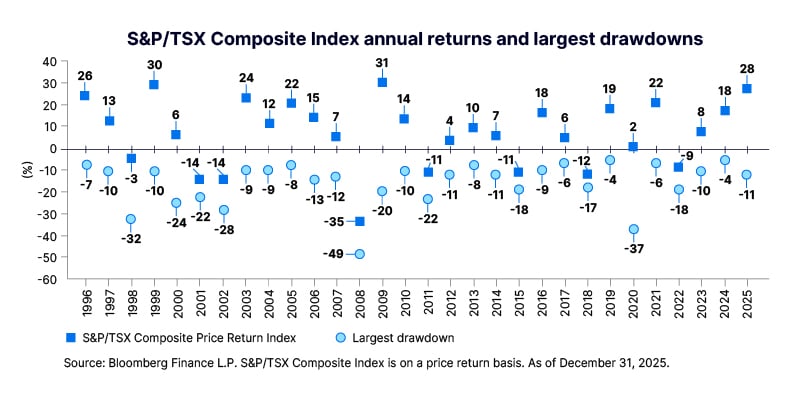

Figure 1: Market drops are normal: Long-term returns still win - Even in years when markets fell sharply, they often finished higher than where the drop began.

The biggest mistake investors make during volatility

Volatile periods often trigger the urge to act, usually by reducing exposure and waiting for conditions to “settle.” The problem is that markets rarely provide a clear signal when stability has returned. Historically, some of the strongest market days occur during periods of uncertainty, not after them.

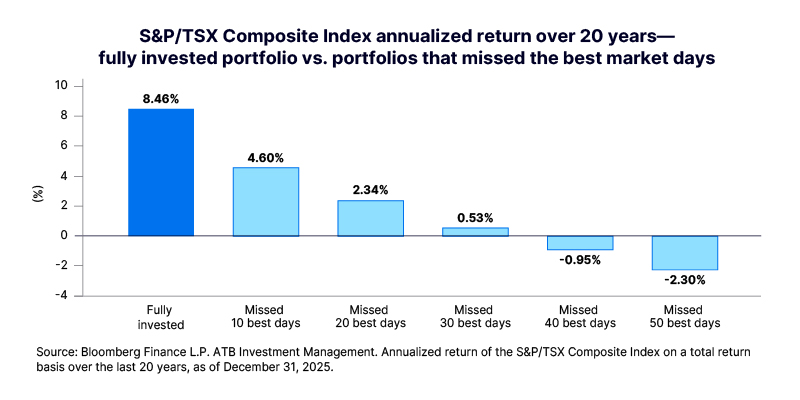

As Figure 2 shows, missing just a handful of those strong days can meaningfully reduce long-term returns. Staying invested avoids the risk of selling low, missing the rebound and re-entering too late.

Figure 2: The cost of trying to time the markets - Missing the market's best days can dramatically reduce long-term returns

Why staying consistent can work, even when markets are bumpy

Investing steadily, regardless of market headlines, removes the pressure to time decisions. By contributing regularly, investors naturally buy more when prices are lower and fewer units when prices are higher. Known as “dollar-cost averaging,” this approach can reduce average purchase cost and help keep investors aligned with their long-term plan.

The approach works especially well when emotions run high. Volatile periods often cause investors to hold cash on the sidelines, waiting to re-enter at an “ideal” moment that rarely arrives. Dollar-cost averaging offers a practical and psychological bridge back into the market, committing smaller amounts on a schedule to keep you moving forward without the pressure of perfect timing.

The discipline also applies to a larger lump sum sitting on the sidelines. Spreading a large amount across several contributions, rather than investing it all at once, gives you a more controlled re-entry. You still put the money to work, but you do it gradually, reducing the risk of investing everything right before a market pullback, while still maintaining forward momentum.

Put your plan on autopilot and remove guesswork

One of the easiest and most effective ways to put this into practice is to automate it. A pre-authorized contribution (PAC) plan takes the guesswork and emotions out of investing by putting your plan on autopilot. Instead of deciding when to invest each time markets move, your plan keeps working quietly in the background. Getting started on a PAC plan is simple:

- Choose an amount you’re comfortable contributing regularly

- Set a schedule that works for you, like every payday or once a month

- Contribute automatically from your bank account into your portfolio

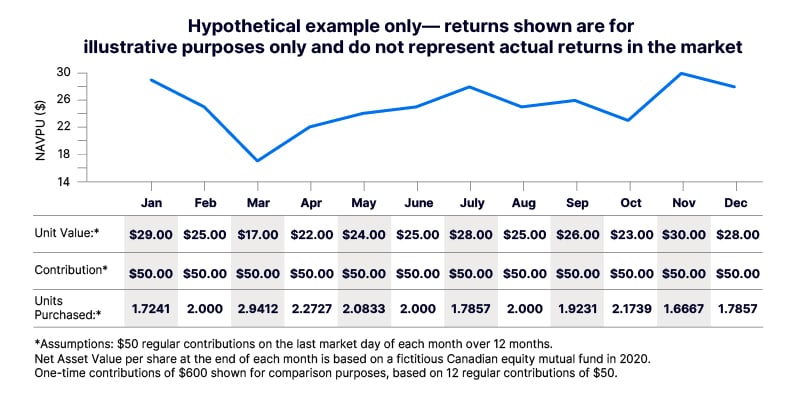

As Figure 3 demonstrates, regular contributions tend to capture more units during price dips which can potentially result in a better overall outcome than a single lump-sum investment made at an inopportune time. Over the long term, discipline—not timing—often makes the biggest difference.

By investing $50/month, dollar-cost averaging captures more units during price dips and results in a gain, vs. investing the same amount all at once at the beginning or highest price of the year.

|

Total units purchased |

Total value at end of year |

Gain/loss |

|

|

Regular contributions of $50/month throughout the year ($600 total) |

24.3565 |

$681.98 |

Up $81.98 |

|

Lump-sum ($600) investment at beginning of the year |

20.6897 |

$579.31 |

Down $20.68 |

|

Lump sum ($600) investment at the highest price |

20.0000 |

$560.00 |

Down $40.00 |

Figure 3: Example

Why diversification matters more than ever

Diversification has always been a good idea, but it’s essential for Canadian investors. While Canada offers strong opportunities, its equity market is heavily concentrated in financials, energy and materials. That concentration can lead to portfolio imbalances during sector-specific downturns.

Global diversification can help investors access more opportunities in:

- Technology, health care and renewable energy

- High-quality global dividend payers

- Faster-growing international and emerging markets

While diversification does not prevent volatility, it spreads risk and can help create a smoother return profile over time.

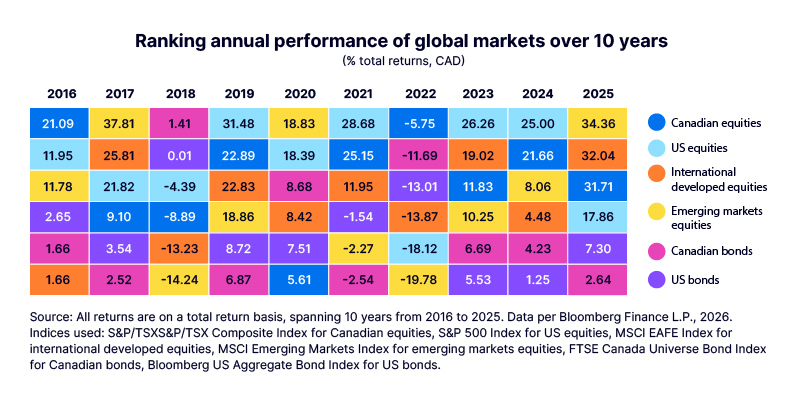

Figure 4: The importance of global diversification: Market leaders rotate - Annual returns across six major asset classes show that leadership rotates from year to year, reinforcing the case for a diversified portfolio that doesn't rely on picking last year's winner.

Navigating volatility: How ATB Funds can help

One way to see how the key principles of navigating volatility come together is through real-world solutions. ATB Investment Management (ATBIM) solutions are designed to manage volatility thoughtfully and deliberately, rather than attempting to avoid it altogether. The strategies offer:

- Diversification across regions, styles, income types, sectors and investment managers

- Global exposure that reaches beyond Canada’s markets

- Professional oversight by ATBIM’s Multi-Asset Strategies Team, complemented by expertise from trusted global investment managers

Volatility is normal. A structured plan matters more

The conditions driving today’s uncertainty may feel new, but the experience of navigating uncertainty is not. Successful long-term investors rely on principles that have stood the test of time:

- Volatility is normal and historically long-term growth has been realized

- The goal isn’t to predict markets; it’s to have a plan and stick to it no matter what the markets do

- Staying invested through the noise is better than waiting for perfect clarity

- Diversification isn't just a strategy; it's a potential buffer between you and your emotions

- Downturns historically become chapters in a much longer story of recovery

The investors who look back on this period with confidence will likely be the ones who held a structured, principles-based plan together, even when it felt hardest to do so.

Want to learn more about how to navigate volatility with confidence while staying on track toward your goals? Explore ATB Funds, designed to help manage volatility through a diversified, professionally managed approach.

ATB Investment Management Inc. (ATBIM) is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the ATB Funds. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice, and ATBIM does not undertake to provide updated information should a change occur. The information in this document has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATB Securities Inc. do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

The material in this document is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any investment. This document may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.