IPM Economic & Market Summary Q1 2026

In the face of the "Global Economic Fog" and the market "whiplash" that defined the first quarter, our priority remains steadfast: aligning our portfolios with our clients long-term investment goals. Our Q1 investment summary breaks down the current market and economic forces impacting the global economy.

At a glance: Global economic fog

Global markets experienced a period of "whiplash" during the first quarter of 2026, primarily due to a convergence of several major events. Significant policy shifts from the US administration, including changes to tariffs and tax cuts, contributed to this volatility. However, the most considerable impact came from the war in Iran and the resulting closure of the Strait of Hormuz.

- The global economy is caught between a technology-led expansion and geopolitical-driven inflationary shocks.

- As a result, global equity markets were increasingly volatile, repricing expectations around energy prices and interest rate expectations for the remainder of 2026.

- Canadian stocks outperformed their global peers as energy and material stocks had another strong quarter, highlighting Canada’s role within a portfolio as an effective hedge against global energy shocks.

Total returns in Canadian dollars terms for quarter ending March 31, 2026:

|

Major Market Indices* |

Quarterly return |

|

S&P/TSX Composite Index |

3.94% |

|

S&P 500 Index |

-2.60% |

|

MSCI EAFE Index |

0.55% |

|

FTSE Canada Universe Bond Index |

0.23% |

Economic summary

Global growth remained intact in the first quarter but became increasingly uneven across regions. Inflation progress has also stalled, with renewed energy shocks and geopolitical tensions shifting central banks back toward a more cautious wait-and-see approach to rates. These shocks have further magnified the K-shaped bifurcation, with lower income households bearing the brunt of higher energy and food prices. The duration of the conflict in Iran will be the primary determinant of the impact on supply chains, food and energy prices, and the broader global economy.

US economy: Policy-induced volatility

The US economy began 2026 with significantly less momentum than anticipated. The first quarter brought a harsh reality check: slowing growth coupled with rising prices.

The impact of January’s “One Big Beautiful Bill Act” (OBBBA) was negated almost immediately by a 15% tariff surcharge implemented in February. The overall picture is one of slowing momentum, with the economy cooling faster than expected alongside a complicated spike in inflation.

Key indicators reflect this trend. The Bureau of Economic Analysis revised its second estimate for Q4 2025 GDP down sharply from 1.4% to 0.7%. Furthermore, the labour market was weaker last year than initially reported; while the unemployment rate remains at 4.3%, the underemployment figure (those working part-time but want full-time work) is at a seven-month high.

The US Federal Reserve left rates unchanged at its March meeting as it navigates its dual mandate of price stability and full employment. Despite global uncertainty and rising prices, the US consumer continues to spend. In our view, the data is indicative of moderating growth rather than a total stall. The probability of a near-term recession remains low, unless the economic fallout from the war in Iran escalates further.

Canada: Resource resilience vs. demographic shift

Canada continues to face productivity issues despite the “build, baby build” narrative. Following a mild GDP contraction in Q4, Canada saw its first population decline in decades—a 0.25% drop in Q1. The population slowdown aided our inflation but has hurt our workforce as we saw unemployment rise to 6.7%.

The Bank of Canada also left interest rates unchanged, and Tiff Macklem explained: “We continue to expect the Canadian economy to grow modestly as it adjusts to US tariffs and trade policy uncertainty, but recent data suggest that near-term economic growth will be weaker than anticipated in January.” As of March, ATB Economics is forecasting 1.50% growth for Canada in 2026 and 2.70% for Alberta1. Alberta’s higher growth is not purely tied to increased energy prices. Our province continues to see population growth due to more affordable housing and strong job growth.

Global outlook

Economies outside of North America faced the brunt of higher energy prices as net importers. The Eurozone is facing stagflationary risk as it navigates slower growth and higher prices. Both the European Central Bank and the Bank of England held interest rates steady at their March meetings, but acknowledged the significant impact of the closure of the Strait of Hormuz. The UK has even hinted at the potential need for an interest rate increase.

Japan saw its inflation cool while Japanese consumers are seeing real wage growth and increased domestic spending. In contrast, China is experiencing a slowdown, with government officials setting one of their lowest GDP targets in decades (4.5% to 5%)2.

Market performance

Volatility is back to start the year, with bonds and equities both repricing expectations for the year.

Equity summary

US corporate earnings continue to be strong with the focus once again on AI hyperscalers and explosive capex spending. Despite surpassing earnings expectations, Microsoft shares fell over 10% in a single day as the company faced pressure from investors on their capex spending. The narrative around AI also shifted from “who has the best chips” to “who has the land and power to run them”. We have observed that major tech CEOs have recently highlighted electricity and utility constraints as primary hurdles.

The US stock market has faced headwinds so far in 2026. The dominant themes are investor fatigue over AI spending and caution over large-cap valuations. Consumer discretionary stocks were also impacted by the 15% tariffs on imports. Consequently, there was a rotation into the value factor and sectors like financials and industrials, which will tend to benefit from higher-for-longer interest rates.

The Canadian stock market ended the quarter ahead of its international counterparts, bolstered by a strong rally in both gold and energy, and record profits for Canadian banks. While the precious metal is up 9.60% for the year3, gold prices faced considerable pressure in March. This monthly drop may be attributable to investors engaging in profit-taking amidst market stress or shifting capital into bonds to capture higher yields.

European stocks are now trading at higher valuations, necessitating a strong earnings cycle to justify the increase. However, the unexpected spike in oil prices and uncertainty surrounding tariffs pose risks, potentially squeezing company margins and impeding overall growth. Conversely, Japan's stock market has been boosted by Prime Minister Takaichi's stimulative economic policies, providing a favourable environment for equities.

Fixed income summary

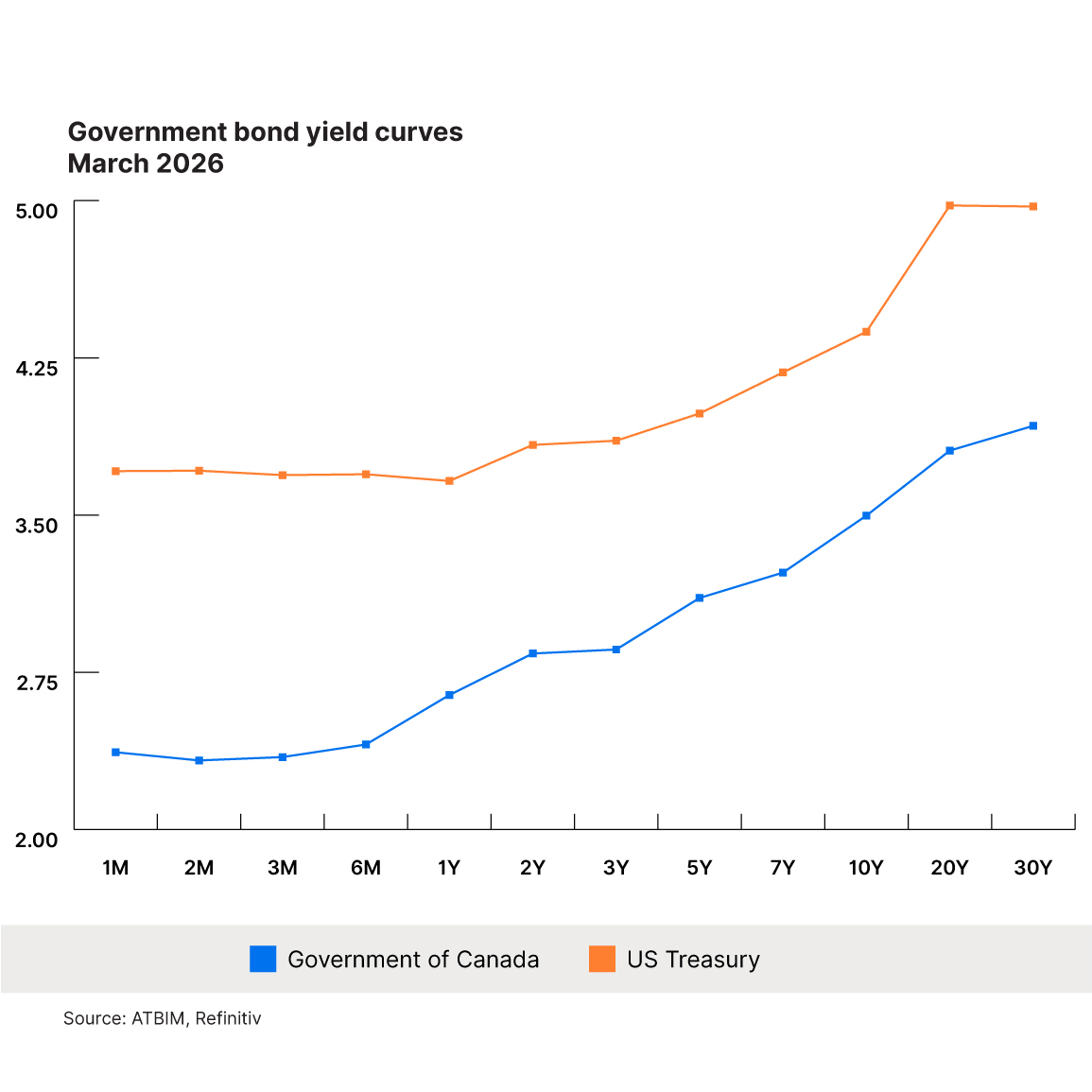

North American credit markets continue to offer attractive income opportunities. The short end of the yield curve has declined in both Canada and the US (relative to a year ago), a direct result of central bank policy and forward-looking market expectations for rate cuts. The current steepening of the North American yield curve is atypical; the lift on the long end is driven by persistent fiscal pressures, heightened inflation uncertainty, and elevated term premiums.

Canada’s yield curve remains comparatively lower than the US, reflecting a more growth-constrained economic environment that limits the rise in long-term yields. Consequently, Canadian fixed income offers a more stable, income-oriented exposure.

Credit spreads remain compressed, signaling market confidence in a soft landing scenario. However, we believe this leaves minimal room for error should economic growth decelerate more sharply. In this dynamic, fixed income provides enhanced income potential, but necessitates the active management of duration, curve positioning, and credit risk amidst an environment of structurally higher volatility.

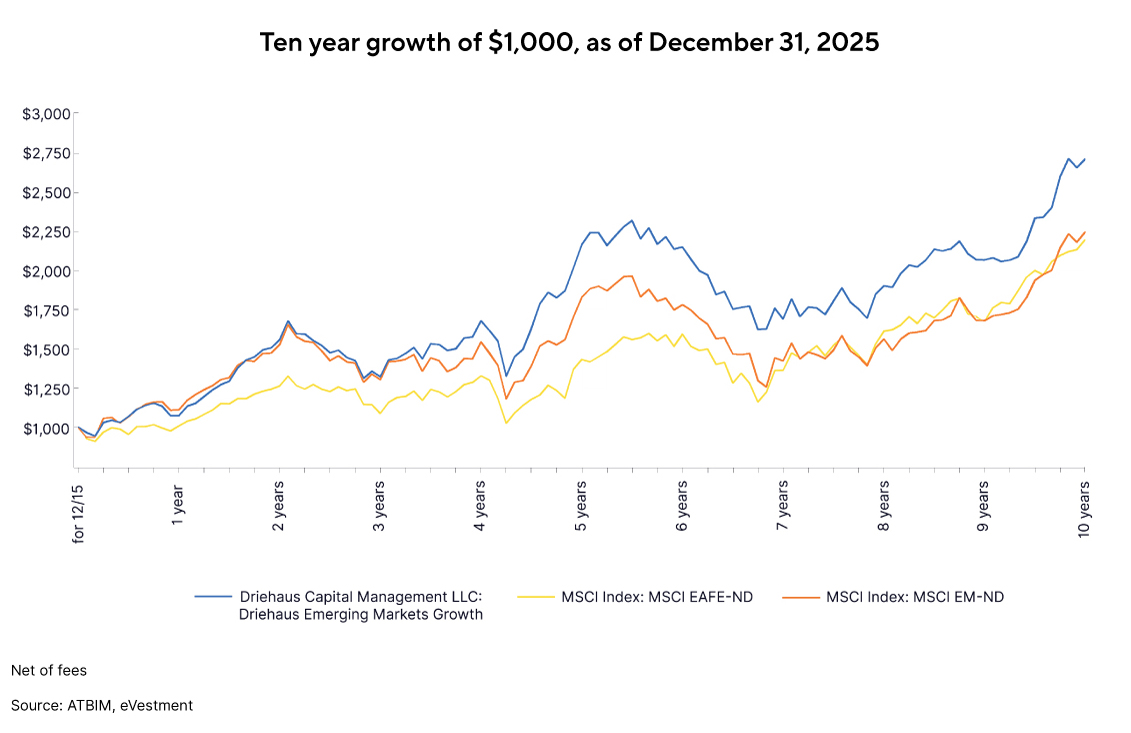

Sub-Advisor highlight: Driehaus Capital Management

Last year, we made the strategic decision to broaden our equity exposures by partnering with four additional institutional-caliber managers. This move was aimed at enhancing our return potential, improving risk management, and positioning our portfolios to perform well across a wider variety of economic scenarios.

One of the equity managers added was Driehaus Capital Management and its Emerging Markets Growth Strategy. We believe this strategy is an excellent choice for a core exposure to Emerging Markets (EM) equity due to its strong diversification, typically holding 80-120 securities. In addition, this broad diversification also offers risk management in the highly volatile EM landscape.

This strategy can create a resilient portfolio across various market cycles by combining four distinct growth profiles:

- Dynamic: High-growth companies and market disrupters.

- Cyclical: Businesses sensitive to economic conditions.

- Recovery: Turnarounds and deep cyclical plays.

- Consistent: Quality compounders.

Driehaus incorporates macro factor analysis into security selection—a crucial element for EM markets—and benefits from a stable portfolio management team. The strategy offers attractive risk attributes and complementary factor exposures. Over the past ten years, the strategy has provided growth above the passive emerging markets index with lower volatility.

What it means for you

Portfolio actions taken

Market volatility and return asymmetry necessitate a proactive approach to portfolio positioning.

Fixed Income

- Our current strategy prioritizes high-quality credit, where we see compelling value in the 5- to 10-year segment of the yield curve. We are deliberately avoiding extending duration given persistent inflation uncertainty and increased interest rate volatility at the long end.

- We continue to favour government issuances to enhance portfolio stability.

Equities

- Our lower-volatility strategies have successfully navigated the challenging global economic landscape, each adding value through its distinct strategies.

- Our active sub-advisors remain focused on identifying companies with the intrinsic resilience to withstand economic dislocations.

We have been actively rebalancing portfolios with the goal to maintain a disciplined and robust investment strategy.

Forward outlook

In the face of the "Global Economic Fog" and the market "whiplash" that defined the first quarter, our priority remains steadfast: aligning your portfolio with your long-term investment goals. At its core, this is a commitment to the disciplined balance of preserving capital while compounding it over time.

In uncertain times, successful execution is not a matter of luck; it is a matter of portfolio architecture. We believe that a resilient portfolio is built on two foundational pillars:

- Preparation over prediction: We do not build strategies based on guessing geopolitical outcomes or short-term trends. Instead, we prepare for them by identifying strategies with intrinsic resilience and maintaining a proactive approach to portfolio positioning.

- Strategic insulation: By diversifying across high-quality credit and institutional-caliber equity managers, we provide a potential buffer against the downside risks of energy shocks and policy-induced volatility.

We are not waiting for the fog to clear to take action. Through active rebalancing and a focus on capital preservation, your portfolio is not just surviving the current environment, but is architected to be in a position to thrive in the years ahead.

1 https://www.atb.com/company/insights/alberta-economic-outlook/

2 BCA Research

3 Bloomberg

ATB Investment Management Inc. (ATBIM) is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the ATB Funds. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice, and ATBIM does not undertake to provide updated information should a change occur. The information in this document has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATB Securities Inc. do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

The material in this document is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any investment. This document may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.