Building resilient spending policies in uncertain times

How can Canadian non-profits and institutional investors ensure financial sustainability amid economic uncertainty? ATBIM’s Institutional Senior Portfolio Manager, Jeremy King, CFA, CPA, CMA, CFP believes that thoughtful spending policies can help organizations maintain stability, preserve capital, and support their missions through volatile times.

Strengthening financial stability in an uncertain world

As we progress through 2025, Canadian organizations, particularly non-profits and institutional investors, face significant economic uncertainty. Shifting global trade policies, geopolitical tensions, inflationary pressures, and financial market volatility contribute to an unpredictable environment that demands careful financial stewardship.

The US administration continues to cause concerns over protectionist trade policies with ongoing threats of tariffs and policy shifts disrupting Canada’s trade relationships. At the same time, rising global debt levels, slowing economic growth in major economies, and geopolitical conflicts continue to weigh on investor confidence. Energy price volatility, instability in regions like Eastern Europe and the Middle East, and uncertain monetary policies from major central banks further complicate financial planning.

For Canadian non-profits and institutional investors, this backdrop underscores the need for prudent financial governance and adaptable spending policies. Organizations must ensure their financial resources are sustainably managed, resilient to market fluctuations, and aligned with long-term mission goals. A well-structured spending policy serves as a critical tool in managing volatility, helping institutions preserve capital, manage risk, and maintain stable funding regardless of external economic conditions.

Best practices in spending policies for non-profits and institutional investors

A disciplined approach to spending is vital for organizations relying on endowment or investment income. Implementing effective spending policies can ensure financial stability while fulfilling organizational missions.

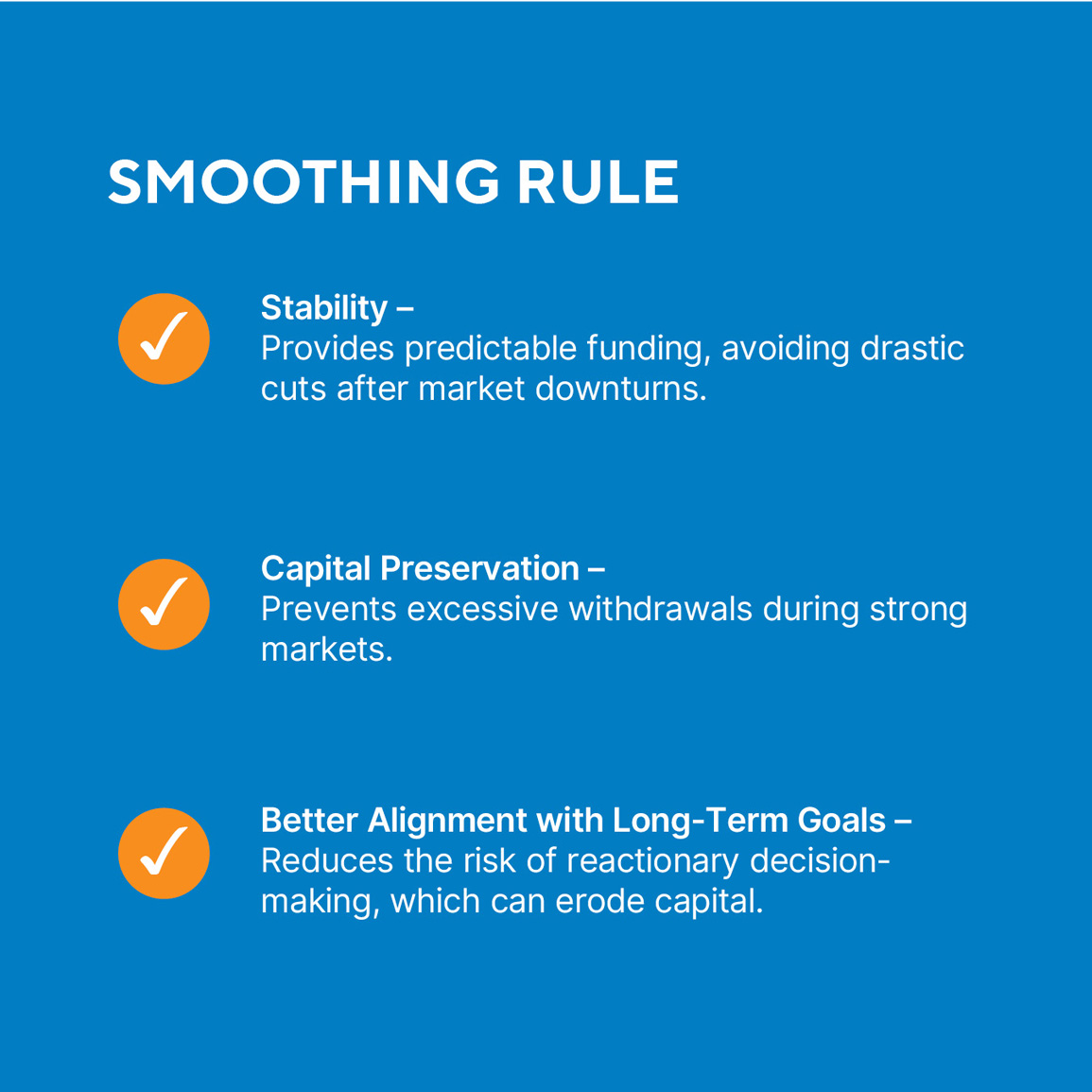

1. Adopting a smoothing rule: A moving-average spending rule, which calculates distributions based on a rolling average of portfolio values over multiple years (e.g., three to five years), reduces volatility in annual budgets and prevents spending from being dictated by short-term market fluctuations.

Compared to fixed spending rates, which rely on a percentage of the portfolio’s value at a single point in time, smoothing rules offer several advantages:

Large institutional investors and endowments widely use this approach to maintain stable funding over multiple years.

2. Incorporating flexibility: Integrating contingency clauses in spending policies allows for temporary adjustments during economic downturns. Some Canadian community foundations1 and institutional investors set upper and lower spending limits to balance current needs with long-term sustainability.

3. Linking spending to long-term return expectations: Spending rates should align with realistic long-term return expectations to preserve capital. Many Canadian foundations and endowments target spending rates that reflect historical real return expectations, typically 3.5% to 4.5% after inflation.

For example, the University of British Columbia (UBC) Endowment2 states that it aims to generate returns sufficient to support annual distributions while preserving long-term capital. Their investment management strategy prioritizes long-term growth and capital preservation to support sustainable distributions.

4. Inflation and interest rate changes: Economic conditions such as inflation and interest rate changes influence portfolio performance and long-term spending sustainability. While inflation erodes purchasing power, spending policies should not be adjusted annually in response to short-term inflation movements. Instead, organizations should:

- Ensure their long-term return assumptions incorporate expected inflation, so the spending rate remains sustainable over time.

- Avoid reactionary spending increases in high-inflation periods. Short-term inflation spikes may not be permanent, and increasing withdrawals could deplete capital.

- Reassess spending rates periodically (e.g., every 3-5 years) to ensure alignment with inflation-adjusted return expectations.

By maintaining a conservative approach that accounts for inflation within return expectations, non-profits can ensure their endowments continue to support their missions without excessive risk.

5. Using a reserve buffer: A well-structured reserve policy ensures non-profits can sustain operations without liquidating assets in market downturns. While every organization’s needs are unique, a common reserve strategy includes:

- Operating Reserves (6–12 months of expenses) – Provides a cushion for short-term financial disruptions.

- Endowment Stabilization Reserves – Helps sustain grant-making when investment returns fall below expected levels.

- Opportunity Reserves – Allows organizations to take advantage of strategic initiatives without impacting core funding.

For example, some Canadian foundations manage their reserves to balance grant-making stability with capital preservation, ensuring that fluctuations in annual investment returns do not disrupt long-term funding commitments3.

By formalizing a reserve strategy and linking it to spending policy, non-profits can proactively manage financial risk rather than reacting to market downturns.

6. Scenario planning and stress testing: Regular scenario analysis and stress testing help organizations anticipate the effects of various economic conditions on their financial health, allowing for proactive policy adjustments rather than reactive decision-making.

Leveraging spending policy as a strategic tool

In times of economic uncertainty, spending policies must evolve to remain effective. Organizations should:

- Regularly review and update spending policies to align with current economic realities.

- Ensure policies reflect both long-term sustainability and mission-driven objectives.

- Engage governance and investment professionals to maintain prudent and adaptable financial strategies.

By treating spending policies as strategic financial tools, organizations can maintain stability while continuing to fulfill their mandates.

Key takeaways: A spending policy checklist for uncertain times

To build financial resilience, Canadian non-profits and institutional investors should:

By embedding these best practices, organizations can strengthen financial resilience, sustain their missions, and manage uncertainty effectively.

Need guidance? ATB Investment Management can help

Every organization’s financial landscape is unique, and navigating economic uncertainty requires a tailored approach to spending policy design. ATB Investment Management’s Institutional Portfolio Management (IPM) team specializes in customized financial strategies for non-profits, foundations, and institutional investors.

For expert guidance on strengthening your organization’s spending policies and investment strategies, reach out to ATB Investment Management today to learn how we can help you build a more resilient and sustainable financial future.

1 Community Foundations of Canada: Key-Governance-and-Administration-Policies_-Template-Guide-for-Canadian-Community-Foundations

2 UBC Endowment: https://treasury.ubc.ca/investment-management/endowments

3 Community Foundations of Canada: Key-Governance-and-Administration-Policies_-Template-Guide-for-Canadian-Community-Foundations

This report has been prepared by ATB Investment Management Inc. (ATBIM). ATBIM is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the ATB Funds. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice, and ATBIM does not undertake to provide updated information should a change occur. The information in this document has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATB Securities Inc. do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

The material in this document is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any investment. This document may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.