Why we don’t hold crypto in the ATBIM funds

Cryptocurrency is trendy but not a fit for every portfolio. We explain the benefits and risks of crypto, and why it’s not part of our current asset mix.

The past few years have seen growing interest from investors in “crypto” or “digital” currencies, sparked by the high (and occasionally spectacular) returns achieved by Bitcoin, the first and most well-known cryptocurrency. Since Bitcoin’s introduction in 2008, thousands of other cryptocurrencies have been created, with names such as Ethereum and Dogecoin, and more recently the crypto exchange FTX, which facilitates crypto transactions and has been prominent in the news for potentially fraudulent activity. In this article, we’ll dive into crypto and its performance since inception and explain ATB Investment Management’s (ATBIM) approach to this currency.

Why we don’t hold crypto in our funds

Before we jump into the history and performance of crypto, here’s a quick summary of our position on this asset.

Because it’s a digital currency, the price of crypto is driven predominantly by supply and demand rather than fundamentals, which makes it a risky prospect because its value is difficult to assess. Certainly, in addition to the outsized positive swings, crypto has also seen negative returns due to its inherent volatility.

Our investment philosophy has a focus on securities that provide tangible quality and future cash flows, managed via sub-advised strategies that also offers a level of downside protection. If we consider Bitcoin to be representative of the cryptocurrency asset class, then it does not meet those attributes. In addition, while the historical performance has certainly shown impressive numbers, its current risk profile doesn’t warrant consideration for an ATBIM investment portfolio.

Let’s explore what makes this currency so risky, and yet so irresistible to investors.

What are cryptocurrencies and why are they so popular?

Cryptocurrencies are a medium of exchange, similar to currencies such as the Canadian dollar, the US dollar, the British pound, and the Euro. As such, their value, or rate of exchange (with another currency), fluctuates with the demand and supply for such a currency. Currencies don’t generate future cash flows, and thus cannot be valued in the same way as traditional assets like equities and bonds.

Due to their existence in the virtual world, cryptocurrencies have no physical or tangible presence, unlike traditional currencies, which can take the form of notes and coins. A $20 Canadian note, issued and backed by the federal government as legal tender, will always be worth $20 in Canada, while a cryptocurrency exists in a digital ledger or database, built using technologies such as “blockchain,”1 and is worth only as much as what people think it is worth. In addition, because a country’s currency is backed by its national government, the supply and demand for a currency like the Canadian dollar can be influenced by the fundamentals of the country itself—the economy, the level of interest rates, political stability, etc. Cryptocurrencies have no domicile to speak of, meaning there is little, fundamentally, to assess the supply or demand dynamics for the cryptocurrency. This means its price, more often than not, is driven by sentiment.

Investor interest in cryptocurrencies has stemmed from the—at times—spectacular returns that a cryptocurrency such as Bitcoin has achieved. For example, in US dollar terms, Bitcoin posted a return of over 1,369% during the calendar year of 2017 alone. Such rises in price have likely been fueled by speculators, fear of missing out (FOMO), as well as a cottage industry that’s emerged to support its (and other cryptocurrencies’) use.

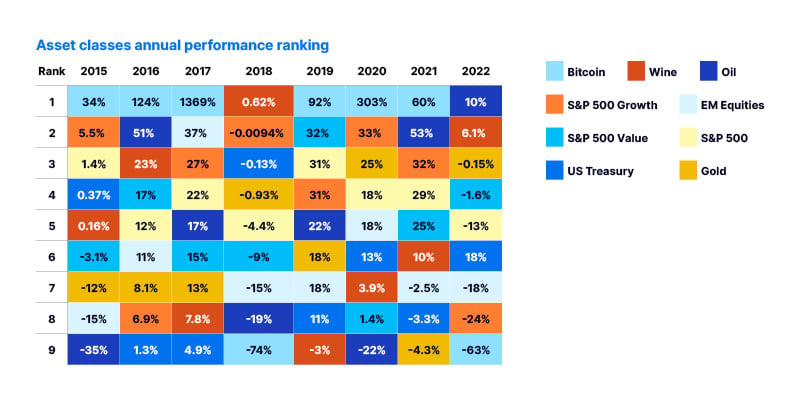

But just as Bitcoin has posted stratospheric returns on occasion, it has also experienced some rapid and extreme drops in price. 2018 saw returns plummet to -74%. The periodic table chart below, which ranks the calendar year return of nine different asset classes (including wine!) for every year back to 2015, shows the volatile nature of Bitcoin’s performance. It has either been the top-performing asset class in a calendar year, or the worst. Note that while -74% may seem like a much lower magnitude than 1,369%, a negative return is naturally capped at -100%. In other words, much of that 1,369% gain from 2017 will have been erased in 2018.

Source: Macrobond

While the total two-year return for 2017 to 2018 is still an impressive 282%, the question arises as to whether a cryptocurrency like Bitcoin belongs in an investment portfolio given such extreme volatility (or swings in price).

Historical performance

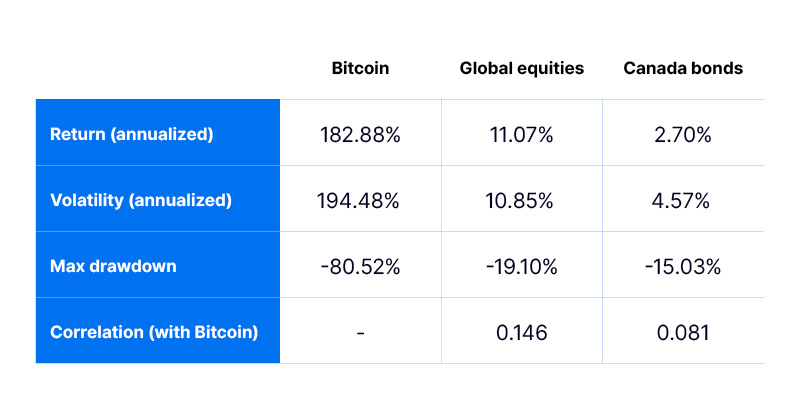

Let’s take a look at the historical return characteristics of Bitcoin (Bitcoin is used for the rest of this article as it has the longest history of any cryptocurrency). The first monthly data point available on Bloomberg is July 2010, so it has a relatively short period for evaluation purposes. Given such a short history, an argument could be made that there’s not enough data to form a solid perspective on how Bitcoin behaves over time. Established asset classes like equities and bonds have many decades of data to work with, and even newer asset classes like hedge funds have data going back to the early 1990s.

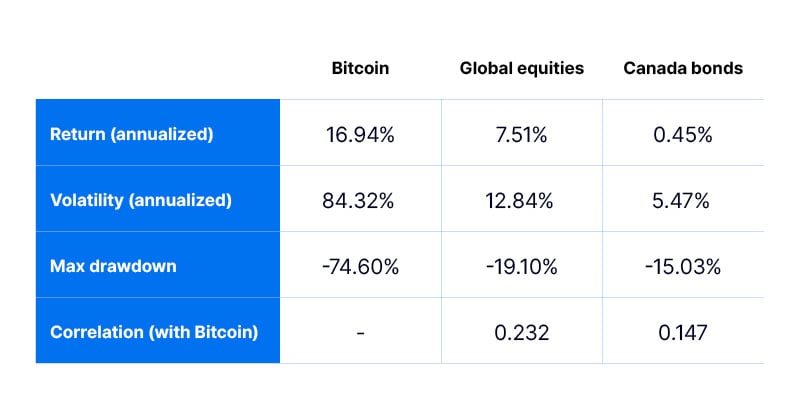

Nevertheless, it’s informative to analyze these return characteristics. The following table uses the MSCI All Country World Index to represent global equities, and the ICE BofA Canada Broad Market Index to represent Canadian investment grade bonds. The period is from Aug. 1, 2010 to Nov. 30, 2022, using monthly returns, all in Canadian dollar terms. Two measures of risk are shown: volatility, defined as the standard deviation of returns, and maximum drawdown, which measures the peak-to-trough decline during the period in question.

Source: Bloomberg

Bitcoin’s annualized return over this period is 183%, which dwarfs the returns from equities and bonds. If we look at the volatility numbers, however, Bitcoin is almost 18 times as volatile as equities, and more than 40 times as volatile as bonds. While the annualized return of 183% is attractive, it begs the question of whether investors would be comfortable with such a bumpy ride.

Furthermore, if we consider the maximum drawdown over this period, Bitcoin experienced an 81% fall in value from July 31, 2011 to Nov. 30, 2011, a period of just four months. The maximum drawdowns for equities and bonds are, comparatively, significantly lower (both occurred over the course of the last two years). Most investors would not be comfortable with an 81% drop in their long-term investments.

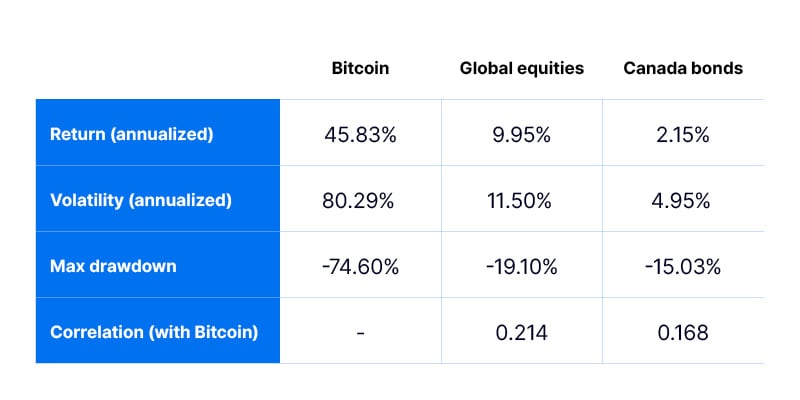

Now, one could argue that the data and access to Bitcoin was limited during the first few years or “startup” phase, so the volatility could be exacerbated given the inefficiency surrounding transactions during that period. So here are the same calculations if we start from January 2014 rather than from Aug. 1, 2010 (ie., Jan. 1, 2014 to Nov. 30, 2022):

Source: Bloomberg

And to take it further, the last five years (60 months), from Dec. 1, 2017 to Nov. 30, 2022:

Source: Bloomberg

In all cases, while still outperforming equities and bonds, Bitcoin’s returns are significantly lower than if we include the early years. Volatilities have fallen dramatically as well, but are still very high at over 80%. Maximum drawdown also remains very high, with a 13-month period (Jan. 1, 2018 to Jan. 31, 2019) where the value fell almost 75%.

One positive from the numbers above is that the correlation of Bitcoin with equities and bonds is low, no matter which period is analyzed, which certainly helps when building a diversified portfolio. This attribute—low correlations with other asset classes—has been one of the selling points of Bitcoin (and cryptocurrencies in general). On the other hand, the return per unit of volatility (ratio of return / volatility) has been falling more recently, or in other words, the amount of return achieved is lower for the same amount of risk.

So, in summary, Bitcoin returns have been high, but one caveat is that the data available for analysis is limited. And, as so frequently disclaimed, historical performance is not an indicator of future performance. The returns have also fallen substantially as the asset has gained more maturity and transactional experience. With respect to risk, volatility is several orders of magnitude higher than both equities and bonds, and as for drawdowns, losses can be quite considerable. Finally, aside from the numerical results, there is little to suggest that, fundamentally, Bitcoin will continue to generate high returns into the future, subject as it is to the forces of supply and demand.

Bitcoin in a portfolio

Unless one can tolerate volatility levels of 80% or higher, or drawdowns of 75%, or is willing to bet that Bitcoin will appreciate over short periods of time (a difficult assignment), the more pertinent question for an investor would be: what impact does an allocation—let’s say, 10%—to Bitcoin have on a long-term investment portfolio?

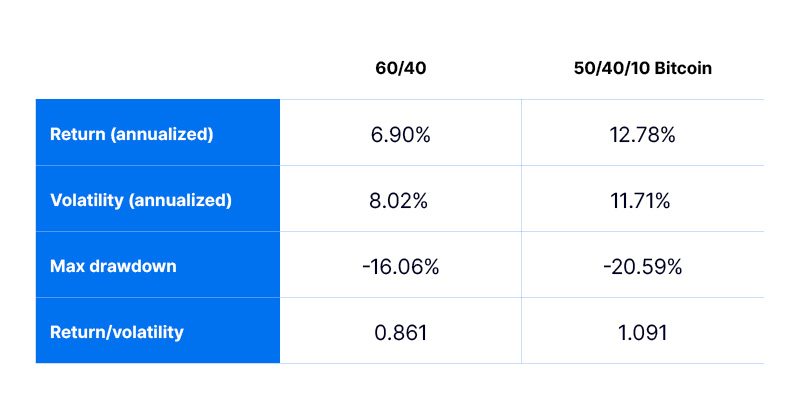

Consider the period from Jan. 1, 2014 to Nov. 30, 2022. The table below compares a typical “balanced” portfolio of 60% equities and 40% bonds, with a portfolio that has a 10% weight to Bitcoin (the allocation is 50% Global Equities, 40% Canada Bonds, and 10% Bitcoin). Rebalancing is assumed to be monthly.

Source: Bloomberg

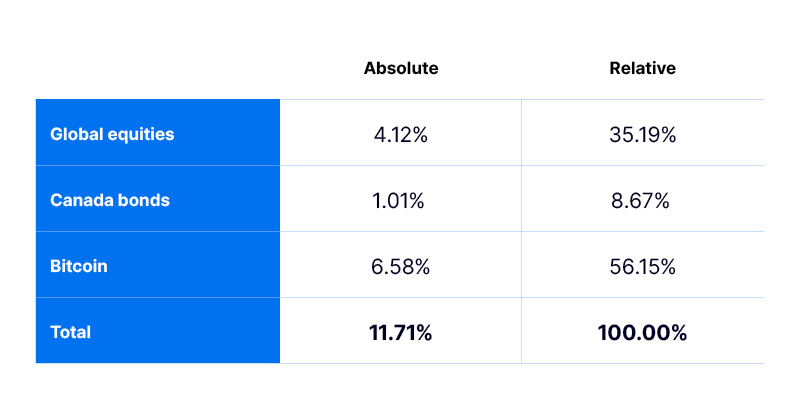

Both the return and volatility jump significantly when adding Bitcoin to the portfolio. The numbers also look attractive from a risk-adjusted basis (using the return / volatility ratio). If we decompose the volatility of 11.71% and see how much each asset class contributes, however, it might give pause, as shown in the table below.

Source: Bloomberg

This shows that even though Bitcoin only occupies 10% of the portfolio, it contributes more than half of the volatility. In other words, it’s the main driver of the portfolio’s risk. For an investor, that’s problematic. For comparison, in a portfolio composed of 10% equities and 90% bonds, the equity portion contributes, on a relative basis, 14% of the portfolio’s risk, much lower than what a 10% weight in Bitcoin contributes.

Future consideration of Bitcoin in the ATBIM funds

Let’s summarize the case for and against Bitcoin’s inclusion as an asset class in an investment portfolio.

The case for:

- Historically higher returns than equities and bonds (caveat: history is not an indicator of future performance)

- Low correlations with equities and bonds.

The case against:

- Intangible, virtual, how does it exist?

- Price driven by supply and demand, rather than fundamentals

- Doesn’t generate future cash flows

- Short history

- Highly volatile, and drawdowns can be substantial

- A small allocation can drive the majority of a portfolio’s risk.

Summary

At ATBIM, we take a longer-term, or more strategic, view when building and managing our portfolios. We assess each asset class on its own merits, as well as what it can add to the portfolio–not only in terms of the potential return, but just as importantly, the potential risks. As we’ve shown above through the data, crypto is far too risky to be considered for our funds, and warrants serious concern for any investor who’s contemplating adding it to their portfolio.

This report has been prepared by ATB Investment Management Inc. (ATBIM). ATBIM is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the ATB Funds, Compass Portfolios and the ATBIS Pools. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice, and ATBIM does not undertake to provide updated information should a change occur. The information in this document has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATB Securities Inc. do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

The material in this document is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any investment. This document may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.