Portfolio managers' commentary

A review of Q1 2023

Positive returns for Q1 despite Silicon Valley Bank volatility.

Summary

- 2023 started out on a positive note, but was ultimately dominated by volatility from persistent core US inflation numbers followed by the concerns surrounding the effects of the Silicon Valley Bank (SVB) failure.

- Despite the volatility, both bond and global equity markets saw positive returns for the quarter as labour markets and company earnings continue to show resilience.

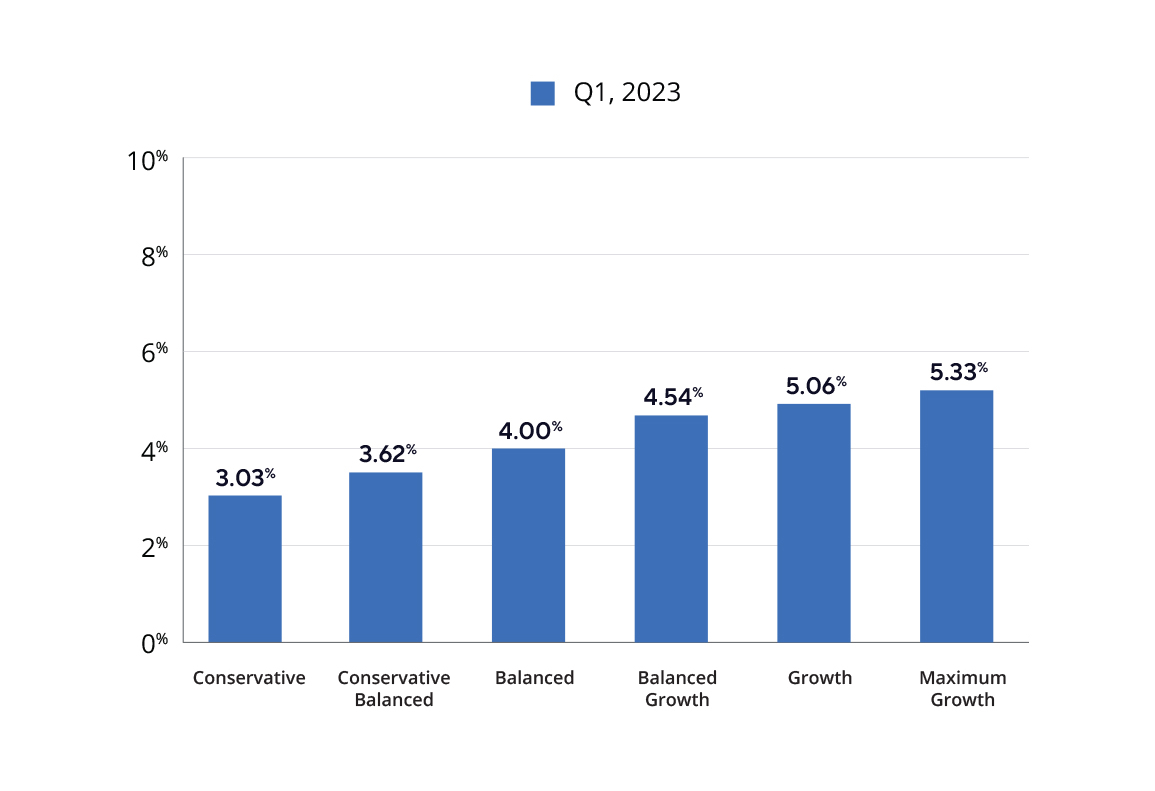

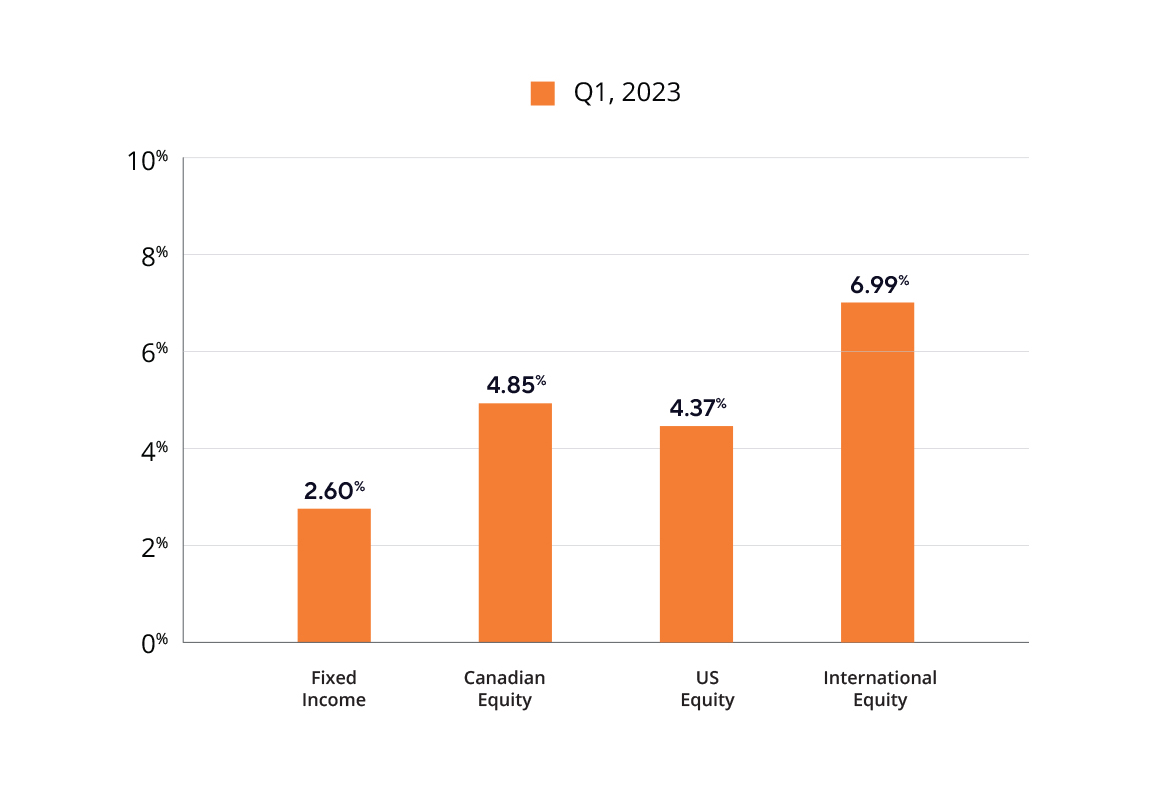

- All ATB Investment Management funds (the funds) saw positive overall performance for the first quarter of 2023. Total returns for the six Compass Portfolios ranged from 3.0% to 5.3%, and the four ATBIS Pools ranged from 2.6% to 7.0%.1

- Overall asset mix targets within the funds over the quarter were unchanged. Activity primarily centred around trimming equities to rebalance as they rose to higher levels towards the end of January. For fixed income, the focus remained on adding to government-backed bonds as well as commercial mortgages that fit our criteria for quality.

Economics

Inflation has continued to moderate through the first quarter of 2023 after peaking last summer. The most recent reading of the consumer price index (CPI), as a measure of overall inflation, showed an annual rate of 5.2% in Canada, and the Bank of Canada (BoC) projects this to decline to around 3% by mid-2023. Year-over-year base effects from falling commodity prices—which also peaked last summer—are likely to be the biggest factor in the BoC’s projections for CPI dropping. The Bank of Canada last met on March 8 and decided to pause at the current 4.5% rate, with the expectation of near-zero real growth over the next few quarters. The US and Eurozone, by contrast, have continued to hike rates with plans for further hikes in the coming months. Common among all policy makers is a focus on seeing further improvement to core inflation measures before signaling a policy pivot. However, labour markets remain tight, and wage growth elevated, which could keep inflation sticky.

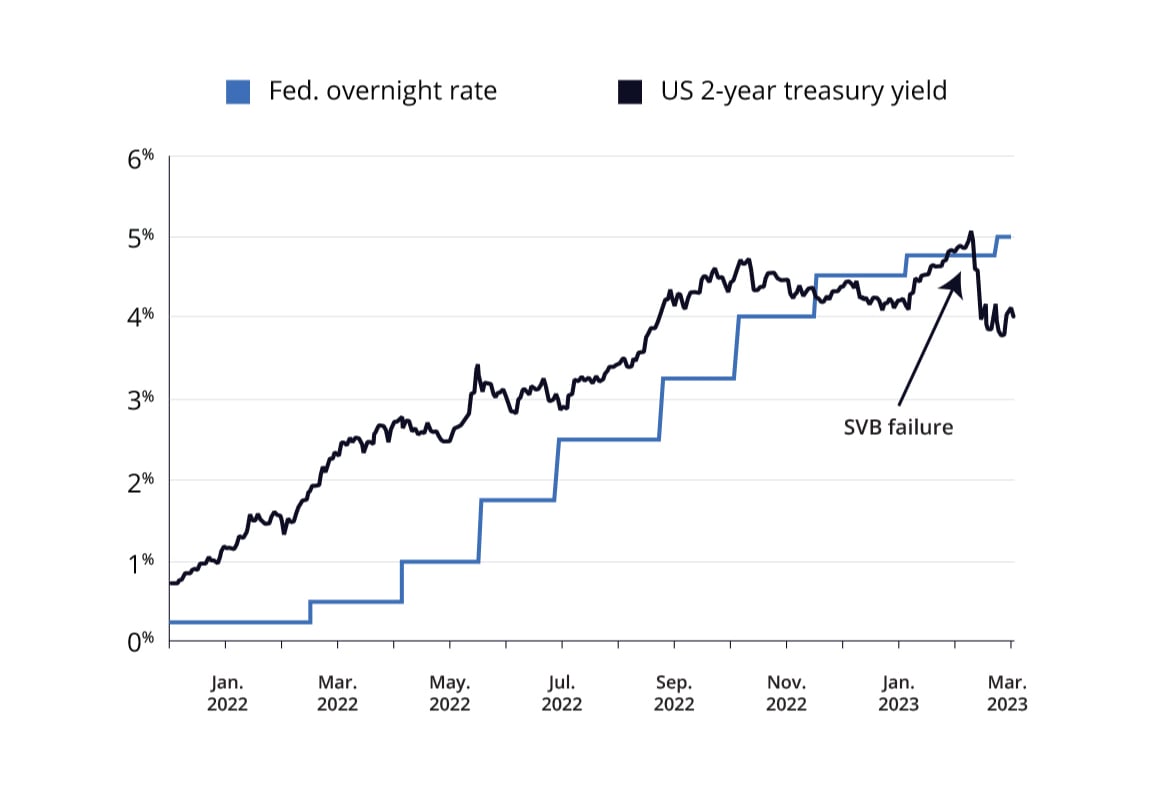

Although inflation is still the key factor for central bank rate decisions, market focus quickly shifted to the impact of rising yields on bank balance sheets as a result of SVB (Silicon Valley Bank, in the US) being placed into Federal Deposit Insurance Corporation (FDIC) receivership. Contagion resulting from SVB’s failure led to significant bond market volatility, with yields falling more than 60 basis points (BPS) in one day,2 where a typical move is no more than five BPS. While a bank failure is usually cause for concern, it’s important to note the unique circumstances surrounding SVB and the government response. Contrary to the 2008 bank failures, a combination of poor interest rate risk management and a highly concentrated depositor base led to SVB’s demise. The backstopping of potential depositor withdrawals by the Federal Reserve through a new Bank Term Funding Program (BTFP) was also key to limiting any contagion within the banking system—ensuring confidence in the banking system is vital. Given the nature of SVB, this is likely an isolated incident, although there will certainly be more scrutiny of smaller regional bank balance sheets as a result.

While the Federal Reserve (Fed) is likely to consider the impacts of further rate hikes to the financial system, the Fed has reiterated its focus is still on taming inflation. As banks have yet to see a material deterioration in their loan books from rising interest rates, it's difficult to make the case for the Fed to pause until it sees a sustained decrease in core inflation and a moderation of the tight labour market.

Fixed-Income Markets

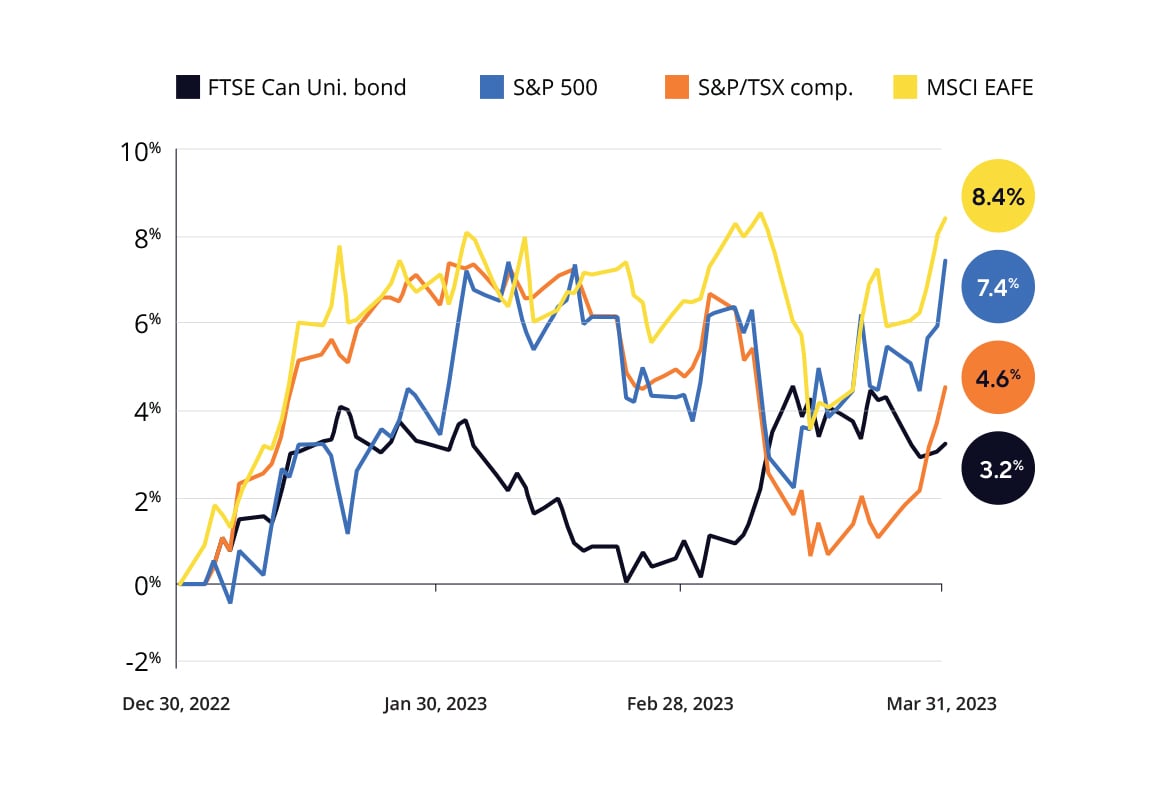

Following a rough year, fixed-income markets had a positive first quarter with yields dropping around 33 BPS overall, resulting in a 3.2% return3 by the end of March.

January saw Canadian bond yields fall as a result of the BoC raising rates by 25 BPS and signaling a possible pause as headline and the bank’s core measures of inflation continued to fall. As Canadian markets are joined at the hip with our neighbours to the south, higher-than-expected combined headline and core US inflation and a hawkish Fed sent yields up during February, despite a pause from the BoC and falling Canadian inflation.

March saw the return of bonds acting as a ballast for portfolios, with the fallout from SVB causing yields to drop roughly 50 BPS. This resulted in bonds once again protecting the downside for balanced investors on days where equities fared worse. Spreads fell and rose more than one standard deviation (25 BPS), although they ended the quarter slightly above where they were at the beginning of the year, highlighting the volatility of credit markets brought on by the SVB failure.

Fed overnight rate vs two-year US treasury yield

Source: Bloomberg

The drop in yields worked in favour for the funds’ fixed-income holdings from an absolute perspective, returning 2.7% for the quarter, but lagging the index4 by about 0.5%. Spreads widened in March but were little changed over the full quarter, and high-yield bonds outperformed overall. The funds’ underperformance was largely due to the shorter duration versus the index.

We continue to focus on maintaining a quality portfolio, while taking advantage of opportunities when presented. As a result of the contagion due to SVB, the viability of Swiss bank Credit Suisse (CS) was called into question, with the Swiss regulators ultimately brokering a deal in which UBS Group AG took control of CS. Before the deal was announced, there was significant volatility in CS bonds, which we were able to take advantage of, and added a number of senior unsecured bonds, at roughly 0.7% of the fixed-income holdings. As these bonds ranked higher than equity and the AT1 capital bonds, which were written down to zero, the yield on the bonds was well worth the risk because they were still supported by the bank’s loan book, and the quality of those assets were not called into question.

Broad equity & Canadian bond total returns (all in CAD terms) - 2023, YTD

Source: Bloomberg

Equity Markets

While equity markets overall were positive this quarter, there was a reversal from 2022 under the surface among sectors. Last year, energy was the star sector in terms of performance, and tech one of the worst. Through the first three months of 2023, energy stocks have declined while tech has seen a significant rebound.

Looking at the individual regions, the funds’ US equity holdings deviated the furthest, returning about 4.5% in Canadian dollar terms over the quarter and lagging the S&P 500 Index by 2.9%. This gap can be attributed to a few things. Less weight in Apple, Nvidia, Tesla, and Meta, none of which are held by the Mawer US Equity mandate, accounted for roughly half the lag. The other half came from an overweight in small- and mid-cap stocks which underperformed large-cap stocks materially in March in the wake of SVB’s collapse. US small- and mid-cap stocks continue to trade at historically wide discounts to large-cap stocks to a degree not seen in more than 20 years.

Canadian and international equities in the funds didn’t see the same relative performance differential to large-cap benchmarks as the US. Canadian equities slightly outperformed the TSX Composite, returning 4.8%. The outperformance stemmed primarily from active energy selection, where the funds hold less cyclical companies, such as pipelines, which saw less downside. Positive selection in other sectors also contributed and helped offset not holding Shopify, the largest positive return contributor to the S&P TSX Composite on the back of a strong recovery similar to US tech companies. Overseas equities were strong through Q1 where that portion of the funds holdings saw returns of 7% for the quarter. Western European stocks in particular were the best performing. Similar to the US, however, small- and mid-cap stocks underperformed relative to large-cap leaving overall returns for the fund slightly lower than that of the MSCI EAFE Index.

Company earnings in all regions are still proving to be resilient and, coupled with the price declines witnessed through 2022, underlying valuations look relatively attractive for the asset class. We maintain our view that equities represent good value, and have the funds tilted in favour of equities as they have been since March 2020.

Compass Portfolios returns - Series A

Total returns

Source: ATBIM

ATBIS Pools returns - Series F1

Total returns

Source: ATBIM

Closing Remarks

While March saw its fair share of market turmoil in the banking sector, overall returns for the month were still positive for stocks and bonds, adding to what have now been two strong quarters in a row for each asset class. From October 2022 lows, the funds’ fixed-income holdings are up roughly 5%, and equities up 15%. Maintaining focus on one's long-term investment strategy through periods like March can be difficult, but the same periods of lowered optimism often coincide with the initial stages of a market recovery—periods that can be lucrative and difficult to make up for if missed.

1 Compass Portfolio Total Returns for series A, and ATBIS FI Pool Total Returns for series F1

2 US 2 year treasury yield from market close on March 10, 2023 to March 13, 2023 fell roughly 0.6%

3 As measured by the FTSE Canada Universe Bond Index

4 Defined by the FTSE Canada Universe Bond Index

This report has been prepared by ATB Investment Management Inc. (ATBIM). ATBIM is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the Compass Portfolios and the ATBIS Pools. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

The performance data provided assumes reinvestment of distributions only and does not take into account sales, redemption, distribution or optional charges or income taxes payable by any security holder that may reduce returns. Unit values of mutual funds will fluctuate and past performance may not be repeated. Mutual Funds are not insured by the Canada Deposit Insurance Corporation, nor guaranteed by ATBIM, ATB Securities Inc. (ATBSI), ATB Financial, the province of Alberta, any other government or any government agency. Commissions, trailing commissions, management fees, and expenses may all be associated with mutual fund investments. Read the fund offering documents provided before investing. The Compass Portfolios includes investments in other mutual funds. Information on these mutual funds, including the prospectus, is available on the internet at www.sedar.com.

Past performance is not indicative of future results. Opinions, estimates, and projections contained herein are subject to change without notice and ATBIM does not undertake to provide updated information should a change occur. This information has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATBSI do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

This report is not, and should not be construed as an offer to sell or a solicitation of an offer to buy any investment. This report may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.