Cryptocurrencies - an update

Given Bitcoin's stellar year in 2023, has ATBIM changed its view on cryptocurrencies?

We posted this article on cryptocurrencies last year, showing why a cryptocurrency like Bitcoin may not be a good fit for our portfolios. The analysis in that article included data up to November 2022.

Given Bitcoin’s stellar year in 2023, has our conclusion changed? The answer is no. While its volatility has generally decreased, it is still a highly volatile asset. As a result, it does not make sense to hold such an asset in our portfolios.

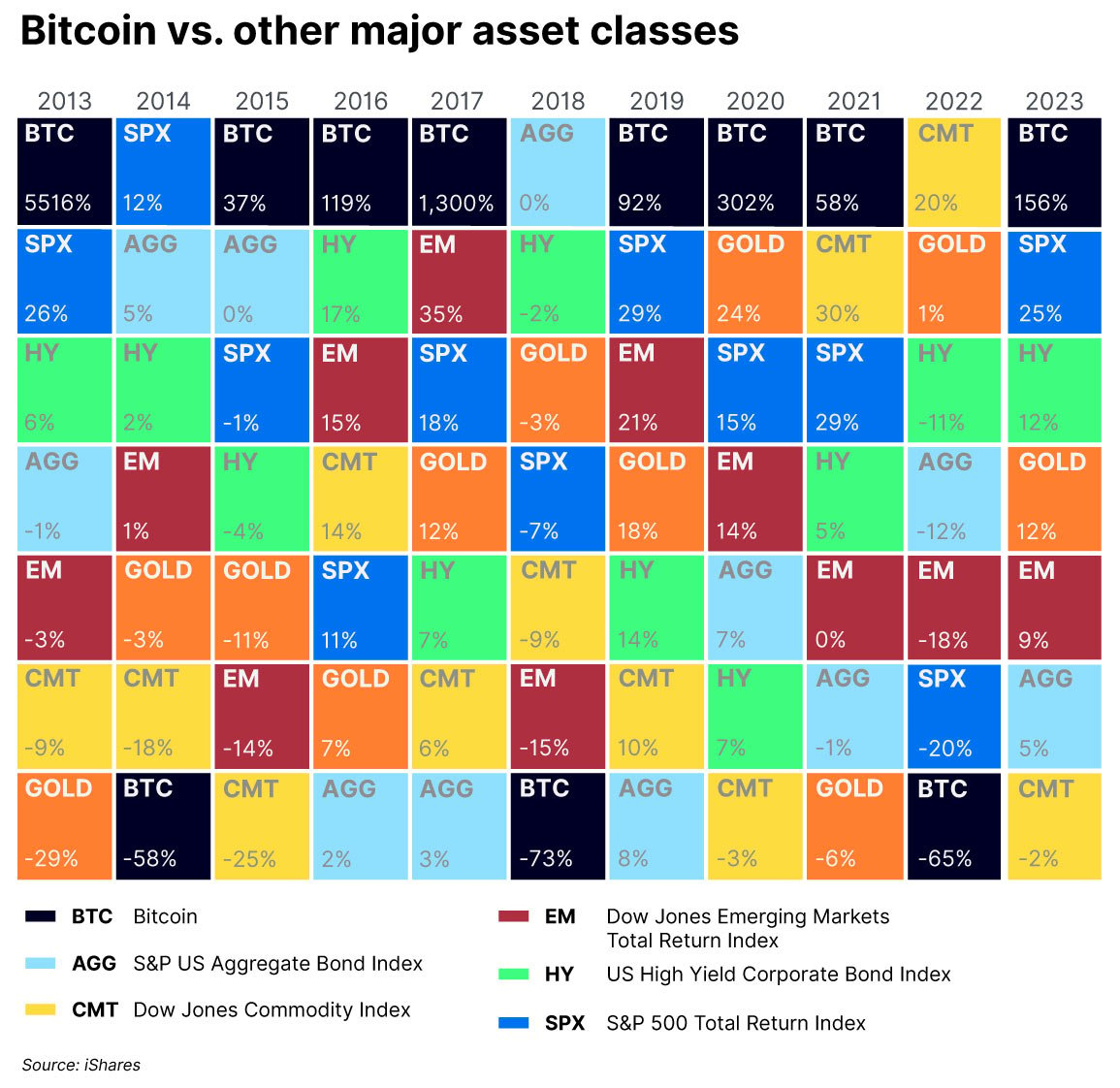

Asset Class Heat Map

Let’s take a look at an updated asset class performance heat map (in US dollar terms).

In 2023, Bitcoin was the top-performing asset class in a sample including US equities, US investment grade bonds, emerging market equities, US high yield bonds, gold, and commodities. The fact remains that Bitcoin is either the top- or bottom-performing asset (given this sample of asset classes)in any given year over this period. While the positive years have outnumbered the negative years, it’s nevertheless been a very volatile ride.

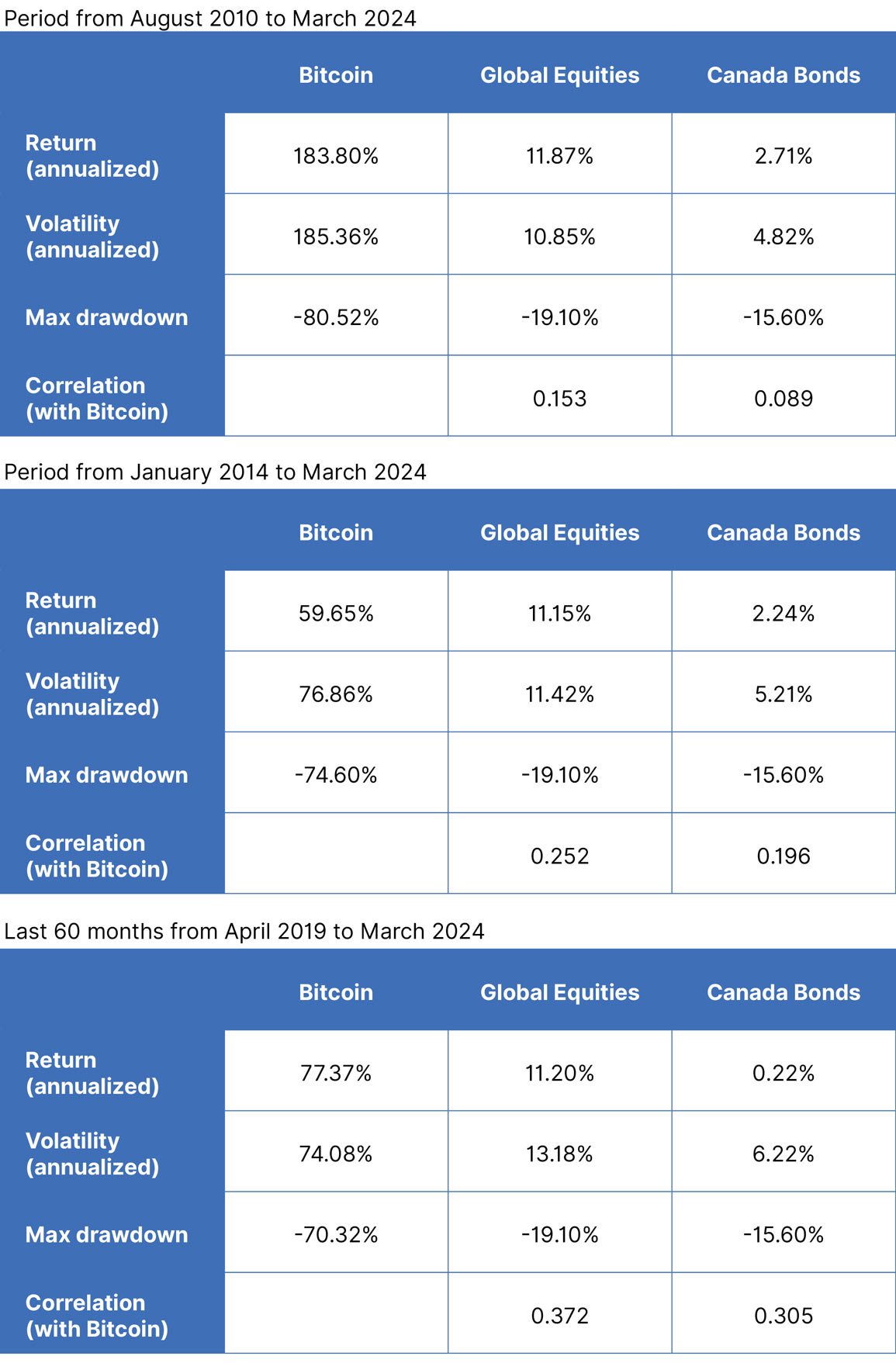

Historical Performance

Let’s revisit the historical performance and volatility numbers given an extra 16 months of data (to March 29, 2024). Global Equities is represented by the MSCI All Country World Index (net), and Canadian Bonds by the ICE BofA Canada Broad Market Index. All values are in Canadian dollar terms, with the data sourced from Bloomberg.

The annualized performance for Bitcoin across these three periods remains very strong when compared to Global Equities or Canadian Bonds. On the flip side, the volatility also remains very high, and the maximum drawdowns are at a much greater magnitude when compared to those two asset classes.

Note that, compared to the original article, the annualized return for Bitcoin over the 5 years to March 2024 results in a much higher number (77.37%, versus 16.94% for the 5 years ending November 2022). This is due to the calendar year of 2018—a very poor year for Bitcoin—falling out of the 60-month window, as well as the inclusion of 2023—a strong year for Bitcoin— joining the window.

Interestingly, the one aspect where Bitcoin offers a benefit for portfolio construction purposes—its “low” correlation with traditional asset classes like equities and bonds—has recently been increasing. This is not to say that correlations between 0.30 and 0.40 (over the last 60 months) are high, but they’re higher than the values over the other two, longer periods.

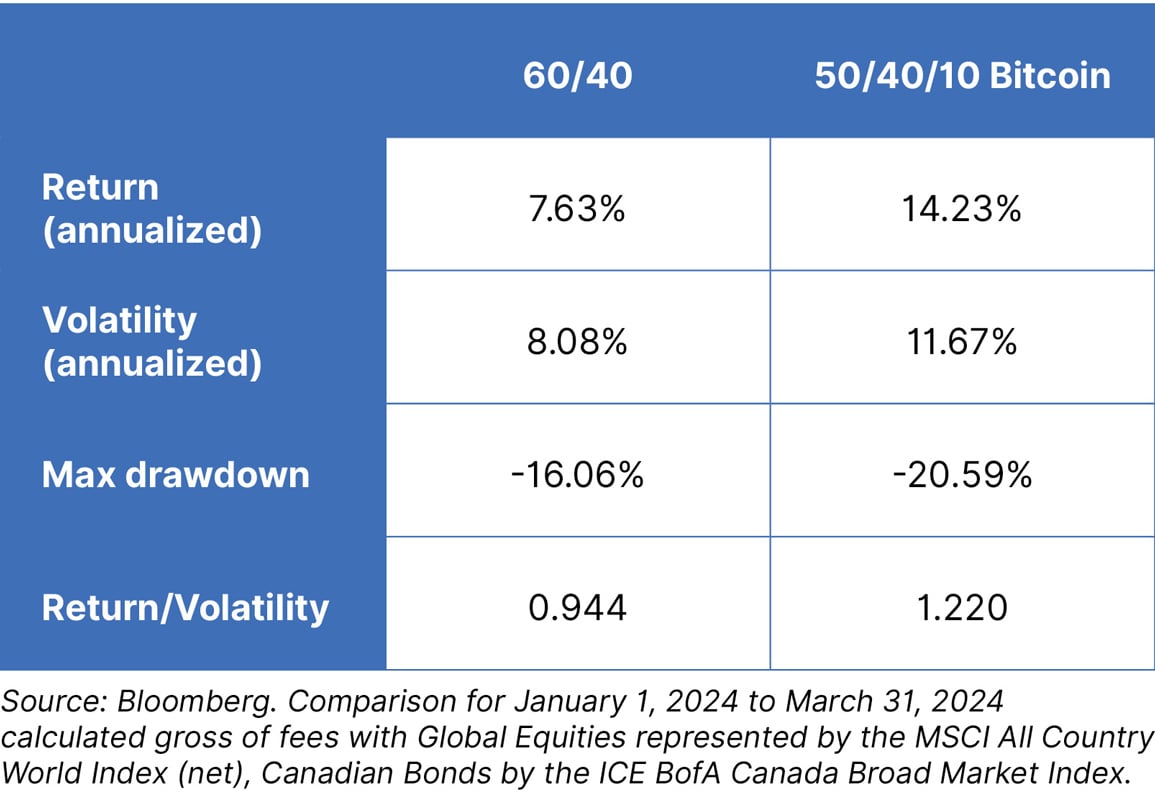

Bitcoin in a portfolio

Using the period from January 2014 to March 2024, let’s compare a typical “balanced” portfolio with 60% Global equities and 40% Canadian bonds versus a portfolio comprised of 50% Global equities, 40% Canadian bonds, and 10% Bitcoin. Global equities and Canadian bonds represent the two traditional asset classes.

The story remains the same. The portfolio with a 10% allocation to Bitcoin has achieved a higher return than the portfolio without, but at a higher level of volatility and a higher drawdown.

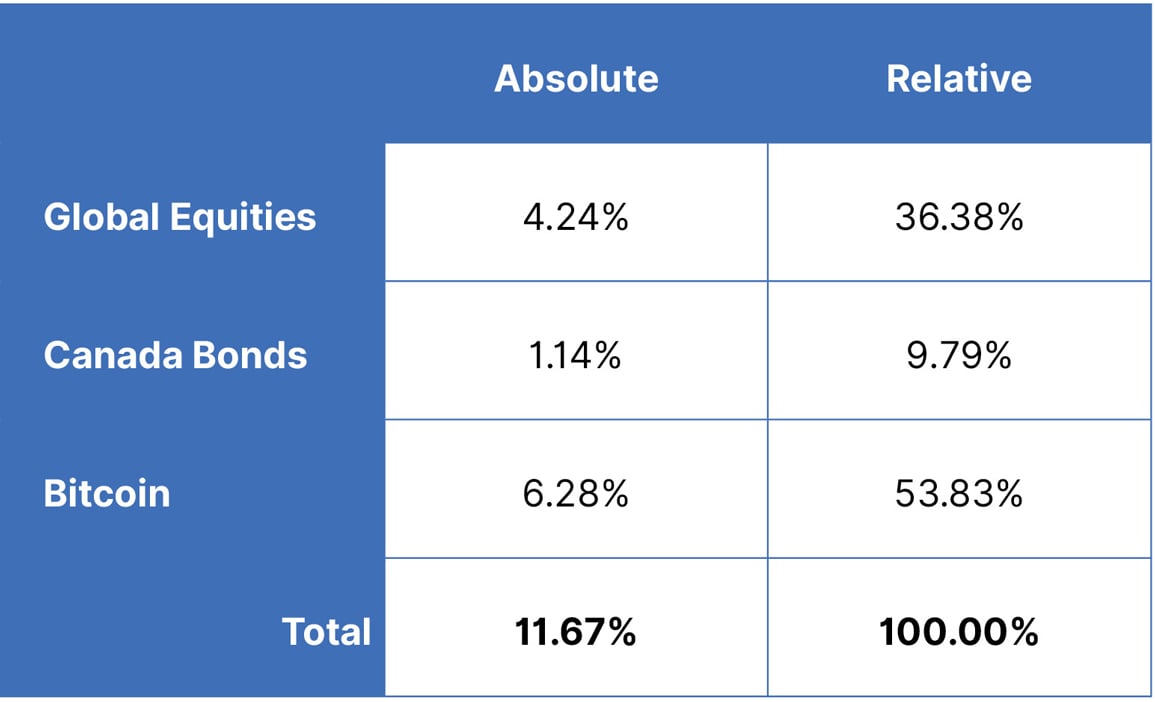

Contribution to Volatility

Decomposing the 50/40/10 portfolio’s individual contributions to risk or volatility over the period from January 2014 to March 2024, we see that Bitcoin remains the dominant contributor, with more than half the portfolio’s level of volatility being driven by the 10% allocation to Bitcoin.

Conclusion

We have updated the performance and risk characteristics of Bitcoin to March 2024. In spite of a strong 2023, Bitcoin remains an extremely volatile asset. It is difficult to value, given that it doesn’t pay any income and lacks fundamentals. Consequently, the price it is traded at depends on supply and demand, and sentiment. As such, these characteristics mean it remains unsuitable for consideration in a long-term portfolio like the Compass funds.

This report has been prepared by ATB Investment Management Inc. (ATBIM). ATBIM is registered as a Portfolio Manager across various Canadian securities commissions with the Alberta Securities Commission (ASC) being its principal regulator. ATBIM is also registered as an Investment Fund Manager who manages the Compass Portfolios and the ATBIS Pools. ATBIM is a wholly owned subsidiary of ATB Financial and is a licensed user of the registered trademark ATB Wealth.

Opinions, estimates, and projections contained herein are subject to change without notice, and ATBIM does not undertake to provide updated information should a change occur. The information in this document has been compiled or arrived at from sources believed reliable but no representation or warranty, expressed or implied, is made as to their accuracy or completeness. ATB Financial, ATBIM and ATB Securities Inc. do not accept any liability whatsoever for any losses arising from the use of this report or its contents.

The material in this document is not, and should not be construed as, an offer to sell or a solicitation of an offer to buy any investment. This document may not be reproduced in whole or in part; referred to in any manner whatsoever; nor may the information, opinions, and conclusions contained herein be referred to without the prior written consent of ATBIM.